Overview:

Lasso regression, a variant of linear regression, incorporates L1 regularization to prevent overfitting by adding a penalty term to the cost function. This technique is particularly effective for feature selection, as it encourages sparsity in the coefficients.

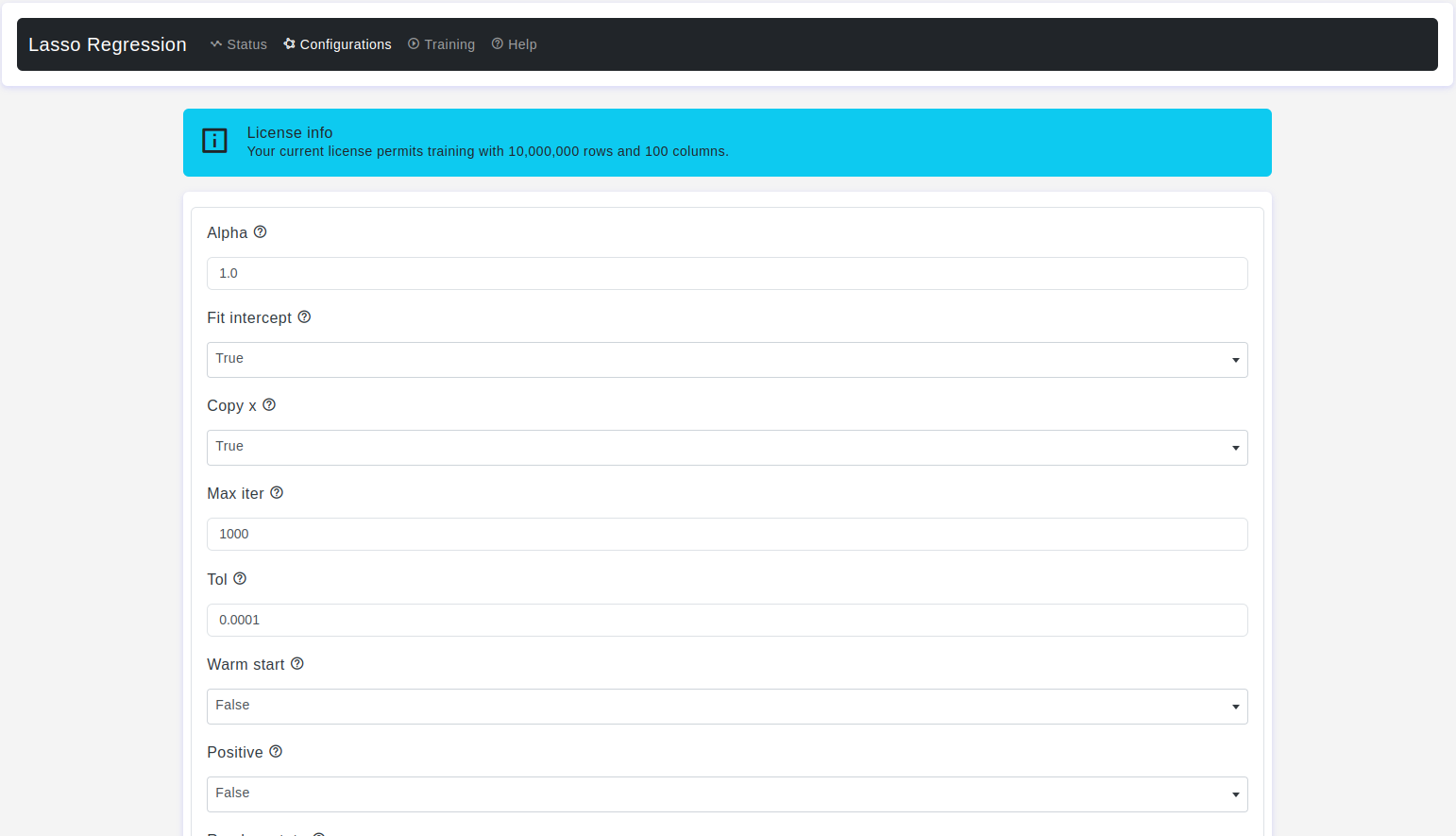

Configurations page:

The Configurations page allows users to adjust various parameters of the lasso regression model. Here are the details:

Alpha

- Default Value: 1.0

- Description: It refers to the regularization strength or regularization parameter. Lasso regression is a linear regression technique that includes L1 regularization to prevent overfitting by adding a penalty term to the linear regression cost function. This penalty term is proportional to the absolute values of the coefficients (slopes) of the independent variables.

- Warning: Must be non-negative.

Fit Intercept

- Default Value: True

- Description: Determines whether to include an intercept term in the regression equation.

Copy X

- Default Value: True

- Description: It refers to whether a copy of the input data (the independent variables) should be made before fitting the model. This parameter is typically used in situations where you want to control whether the original input data is modified during the fitting process.

Max Iter

- Default Value: 1000

- Description: It controls the maximum number of iterations or optimization steps the algorithm is allowed to take while searching for the optimal coefficients.

Tol

- Default Value: 1e-4

- Description: The

tolparameter (short for tolerance) is used to control the convergence criterion for the iterative optimization algorithm. The iterative optimization algorithm in Lasso regression is typically used to find the optimal coefficients that minimize the Lasso regression cost function, which consists of the least squares loss and the L1 regularization term.

Warm Start

- Default Value: False

- Description: It is a boolean parameter that allows you to reuse the solution of a previous Lasso regression fit as the initial coefficients for a new Lasso regression fit. This parameter can be particularly useful when you want to perform a sequence of Lasso regressions with slightly different parameters or when you want to continue the optimization process from a previous fit.

Positive

- Default Value: False

- Description: It is a boolean parameter that determines whether or not the model should enforce that the coefficients (slopes) of the independent variables are strictly non-negative. Setting

positive=Truein Lasso regression ensures that all coefficient values are greater than or equal to zero, effectively constraining the linear relationship between the dependent variable and the independent variables to be positive.

Random State

- Default Value: None

- Description: It is used to control the randomness or randomness-related behavior of the algorithm when there are random elements involved, such as the shuffling of data or the initialization of coefficients.

Precompute

- Default Value: False

- Description: This parameter is a boolean or array-like parameter that controls whether or not to precompute the precompute a specific part of it during the fitting process.

Selection

- Description: It is used to specify the method for selecting which features (independent variables) to include in the model when there are multiple features available. Lasso regression, with its L1 regularization term, has a built-in feature selection mechanism that encourages some of the coefficients to be exactly zero, effectively eliminating certain features from the model.

selection = cyclic: In the cyclic selection mode, Lasso regression iteratively updates the coefficients one at a time in a cyclical fashion. This means that during each iteration, the algorithm selects a single feature and updates its coefficient while keeping the other coefficients fixed. The algorithm cycles through all the features multiple times until convergence. This mode is more memory-efficient and often faster for small to moderately sized datasets.selection = random: In the random selection mode, Lasso regression selects a random feature to update its coefficient during each iteration. This introduces randomness into the feature selection process and can lead to slightly different results each time the model is trained. The random selection mode can be useful in situations where you want to add some randomness to the feature selection process, potentially leading to better generalization. However, it may be slower than the cyclic mode, especially for large datasets.

Test Size

- Description: The

test sizeparameter is used when splitting the dataset into these subsets, and it specifies the portion of the data that will be used for testing. - Default Value: 0.2

Train Size

- Description: The

train sizeparameter is used when splitting the dataset into these subsets, and it specifies the portion of the data that will be used for model training. - Default Value: 0.8

Conclusion

Lasso regression offers a powerful approach to regression tasks, especially when feature selection is crucial. By understanding and tuning its parameters, users can effectively control model complexity and enhance predictive performance.